Central Florida Health and Wellness Magazine Health and Wellness Articles of the Villages

Central Florida Health and Wellness Magazine Health and Wellness Articles of the Villages

Related Articles

IULs are not for everyone, but in some instances, they offer greater flexibility for those who need to plan for multiple events and outcomes.

What is Indexed Universal Life (IUL) Insurance?

What is Indexed Universal Life (IUL) Insurance?

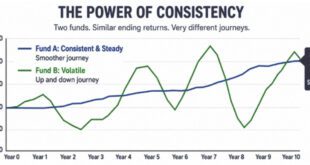

Based on the life of the insured, After a premium is paid, a portion goes toward the cost of the overall insurance. The additional is added to the cash value of the insurance. Not invested in the direct stock, the cash value with interest is credited in an equity index. Written into some policies, the holder can select the percentage to be allocated to one or multiple indexes to credit with the funds.

IULs are evaluated at the end of each month. If the value has increased, the interest is added to the cash value. These gains can be added back to the policy monthly or annually, depending on what the policy holder has decided. If the index goes down, no interest is available to credit.

Why Many People Love IULs

IULs has low premiums because the policy holder is taking more risk.

There is greater flexibility because the policy holder controls how much of the value is risked

Death benefit amounts can be adjusted over time if necessary.

The cash value earned can out-grow the policy and therefore, allow one to stop making out-of-pocket payments.

Because it’s not a stock market investment, the risk is reduced

IULs allow for unlimited contribution, so if a policy holder wants to invest or change allowances, there is no limitations involved.

In regards to long-term care, these come with high dollar investments necessary to pay the 50-upwards of 200,000 per year. Many individuals are thinking ahead and preparing for long-term care with their IULs. A hybrid IUL that allows many retirees to use an alternative to traditional long-term care policies. Hybrid policies are less restrictive. Some hybrid policies offer a death benefit if the policyholder does not use the long-term care benefits.

To find out more about your options, you need an experienced expert.

Cheryl Masters – Mortgage Protection: What You Should Know

If something happens, the last thing a family should have to worry about is making the mortgage payment. Some programs will return all the premium you paid, when the policy expires. Chery Masters is the life insurance agency owner at Masters Life Insurance in association with Family First Life. She is an expert at bridging the gap between the community and well-established insurance agents. Her years of experience and relationships allow her to help you in multiple situations. When it comes to your mortgage and unexpected disruptions, she can help you navigate the situation by supplying you with essential analytics and information, reputable agents, accessibility, and follow through.

Cheryl shares her expertise and advice below:

You are among the fortunate Americans who have made their dream of owning a home come true. Many families have to leave their home due to economic hardship caused by death, disability, or unemployment, so protecting your home for you and your family could be one of the wisest decisions you make.

Consider the following:

If you died, would your family have enough money to pay off the mortgage?

If you were unable to work for an extended period, would your family have enough money to pay the mortgage each month?

If you lost your job, would you still be able to afford your insurance premiums?

Protect your family and home today!

Home Mortgage Series Plus from Americo Financial Life and Annuity Insurance Company (Americo) is a portfolio of term life and universal life insurance products that may help you and your family keep your home and your valuable insurance protection if the unexpected happens.

Please call Cheryl Masters at 877-374-3205 or email her at ms.cheryl.masters@gmail.com for more information or to schedule an appointment.

Cheryl Masters Masters Life Insurance

877 374 3205

Cheryl@CherylMasters.com

www.cherylmasters.com

1 HMS Plus CBO build a cash value that is available to you upon request, less any loans, if the policy is terminated. If the Enhanced Surrender Value Benefit (Cash Back Option benefit) is in effect at the end of the Enhanced Surrender Value Period, the surrender value of the policy will equal the total amount of premiums paid for the base policy, not including any premiums paid for riders. 2 Riders are optional, available for an additional cost and may not be available in all states. 3 Living Benefit Riders are included at no additional cost on HMS Plus 100, 125, and CBO. Subject to state variations.

Americo is authorized to conduct business in the District of Columbia and all states except NY.

Home Mortgage Series Plus (Policy Series 301/302/303/315) and Accidental Death Benefit Rider (Rider Series 2165); Enhanced Surrender Value Rider (Rider Series 2200); Critical Illness Accelerated Death Benefit Rider (Riders Series 2190/2195), Chronic Illness Accelerated Death Benefit Rider (Rider Series 2191/2196), and Terminal Illness Accelerated Death Benefit Rider (Rider Series 2192/2197); Disability Income Rider (Rider Series 2145); Waiver of Premium for Disability Rider/Waiver of Monthly Specified Premium Rider (Rider Series 2158/2158-UL); Involuntary Unemployment Waiver of Premium Rider (Rider Series 2140) are underwritten by Americo Financial Life and Annuity Insurance Company (Americo), Kansas City, MO, and may vary in accordance with state laws. Certain restrictions apply. Consult base policy and riders for all terms, exclusions, and limitations. Cheryl Masters is an independent, authorized agent of Americo.